Flywire's Flywheel

FinTech Fixing to Flip the Faulty Narrative

"We’re not competitor obsessed; we’re customer obsessed. We start with what the customer needs and we work backwards. And that’s the essence of the flywheel." – Jeff Bezos

"No matter how dramatic the end result, the good-to-great transformations never happened in one fell swoop. There was no single defining action... It was a cumulative process — step by step, action by action, decision by decision, turn by turn of the flywheel."

— Jim Collins

“The key to success is finding a flywheel that keeps spinning—and spinning faster—on its own energy.” – Warren Buffett

At ~$11/share, Flywire trades at ~2x sales, ~3x EV/Gross Profit, <9x EBITDA, and ~10x consensus 2026 FCF estimates. We believe this is far too cheap for a company that is capital light, cash rich, and technologically dominant in a couple of specific vertical niches with numerous material growth opportunities (both in cross-sell and new customer acquisition) that seem to be misunderstood by the market.

We believe Q2 (or at worst Q3) will represent the low point in the organic, constant currency revenue growth rate, and that a return to greater than 20% growth is a possibility entering 2026. While investors we speak with are obsessed with current, short-term regulatory and political headwinds (pertaining to student visa limitations and delays), we believe there is significant idiosyncratic developments in the adoption of Flywire’s Student Financial Services (SFS) offering, especially within the UK, that could more than offset a poor macro environment in Canada, Australia, and the United States while simultaneously diversifying the company from annual enrollment risk. If the macro situation in their core education business would just go from miserable-to-meh (as some data points suggest), 20% growth is imminently possible based on our assessment of the opportunity set. Combine that potential top line reacceleration with significant operating leverage, and you have a strong setup to get the stock at least back to where it was prior to their disastrous Q4 earnings call, which would represent over 50% upside.

In a Bull Case, where macro actually reverses to a tailwind and the company reverts closer to their historical growth rates of 25%, we believe the stock could get a multiple closer to other “technology led payment companies in vertical niches” such as Toast (TOST), which trades at ~15x NTM gross profit and over 40x NTM EBITDA, or higher growth payment pure plays like Paymentus (11x NTM gross profit).

In a Bear Case, where the US education market collapses more materially than we expect (or there are new developments in the UK market) and globally there is more of a subdued, longer-term narrative around foreign study, we still feel a price of $9 (or 10x FCF on significantly reduced revenue growth and FCF estimates) is a conservative estimate of intrinsic value given the company’s dominance in education and material balance sheet flexibility for a private equity transaction.

Flywire’s History and Management

Flywire was founded by Iker Marcaide in 2009 (originally called peerTransfer). It is a classic entrepreneurial success story, Facebook style, in that a student saw an issue (in this case, the challenges of paying tuition as an international student) on his MIT campus and built a business around it. Four years later, he handed the reins over to Mike Massaro as the company looked to scale to become a much larger company. Massaro was actually a relative unknown at the time, hired internally as CEO after spending a year as VP of Business Development. Although Massaro did not technically found the company, he is undoubtedly greatly responsible for the eventual breakthrough success of the company, as he presided over funding rounds of $22M in 2015, $100M in 2018, and $120M in 2020, when previous fundraising cumulatively totaled around $16M.

The feedback for Massaro from interviews we have both done and read is very enthusiastic, with this quote from a former employee summarizing the general perception:

“His obsession level is very high. So much so that I have to extract him. He is heavily focused on business and culture.”

Additionally, Mike has a borderline rockstar in CTO David King, who built infiNET in 2006 before selling it to Nelnet and then building it into one of the largest US EdTech platforms before joining Flywire in 2019. In other words, he has been working on simplifying tuition payments online since well before Flywire was even founded and seems to be unanimously thought of as a technical genius. Although the focus of many of the former calls we conducted and read about were geared towards Mike and other management, David’s name kept coming up. Here are a few samplings of comments:

“Dave King is amazing.”

“David King and the entire tech/product team are phenomenal.”

“He is a massive asset due to his PCI connections.”

Although talk can be cheap, we think these comments on management combined with customer comments on the product itself reflect an organization that is far likely to win more business from customers in the future, not less, and gives us more confidence in the next leg of their growth, which is likely to be a greater mixture of upsells and cross-sells, as well as geographic expansion.

Flywire Business Mix

Although the company could do a better job of more regular disclosures around regional and industry revenue exposure, we have pieced together what we believe is close to the industry revenue mix in 2024:

The numbers here tell a story but deserve more context because of the vastly different regional trajectories. Within education, the “shining star” has been the UK (within “Rest of Education”), which has grown so much already that it is now larger than Flywire's US education revenue. Canada has been a severe outlier laggard and represents the heart of the “macro” and regulatory issues the company started going through in 2024. For instance, as we understand it, the significant and draconian rules put in place targeting Indian students in Canada impacted the company by $30M in revenue in 2024 and is expected to hit 2025 revenue in Canada by another 30% (although is now small enough to be less impactful). We expect the overall trends to continue in 2025, with the UK leading growth and Canada lagging.

Outside of Education, it is also a tale of two segments. Healthcare has been a clear laggard since it was acquired in 2020, representing around $30M in revenues that have been stagnant from 2022-2024. Their Travel and B2B verticals, on the other hand, have been going gangbusters (off a relatively small base), growing from around $19M in revenue in 2022 to $76M in 2024. With the recent acquisition of Sertifi, along with ongoing forecasted robust growth, we expect this segment to continue to increase as a percentage of total company revenue.

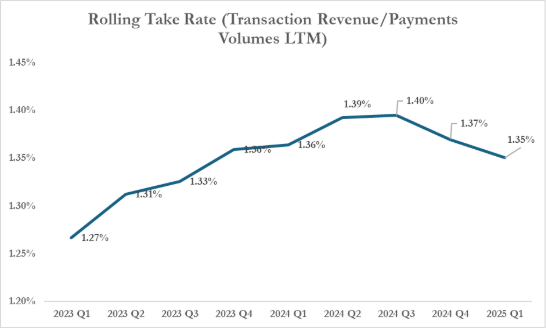

Flywire also reports two types of revenue (Transaction and Platform), like other software/payments companies that have some revenues in payment processing and some revenues more akin to SaaS software.

For Flywire, their Transaction revenues represent revenues from currency conversions and other domestic payment processing, based on a total volume of payments. You can see below this has run in a very tight range between 130 and 140 bps, when looked at on a rolling 12-month basis (to account for seasonality). Transaction revenues still dominate total Flywire revenues, representing around 85% (although this will likely decline as a percentage with Sertfii).

We expect modest downward pressure on take rates as domestic payment processing is likely to grow faster than currency conversion. Offsetting this is that Travel, based on how they account for the revenue, is likely to have a higher take rate.

Given Sertifi is currently 75% SaaS revenues, and that the company continues to focus on growing this revenue stream, we expect Platform revenues to rise (modestly) as a percentage of total revenues.

The Market’s Perception of Flywire and Why the Opportunity Exists

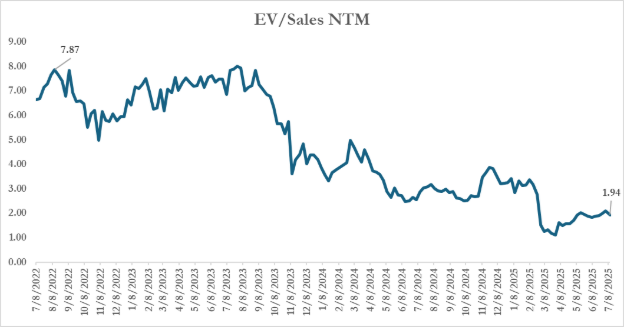

Flywire has been a disastrous investment since their IPO in early 2021, coming out of the gate overcooked at >20x NTM sales while currently trading at 2x. Even if you factor in that virtually all “high flying” software IPOs in 2021 have done poorly, we note a steady and consistent erosion of multiple since the bear market bottom in 2022:

We believe there is a disillusioned investor base, with a bit of a “three strikes and you’re out” dynamic going on.

Strike 1 (2023)

Company issued a secondary in August, 2023, then materially missed the quarter right after the raise, a big no-no. We believe this was the beginning of the end for the previous CFO.

Strike 2 (2024)

Significantly underestimated Canadian headwinds in 2024, resulting in a downward revision to revenue after downplaying the issue initially.

Strike 3 (2025)

Disastrous Q4 earnings call combined with dilutive acquisition (described more below).

We believe “Strike 3” combined with seemingly darker clouds in the US had many of the most loyal investors abandoning the company, specifically those that are growth focused.

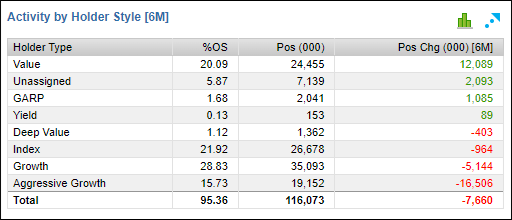

Although there may still be a bit more investor churn to move through, the previous investor base (primarily growth-oriented) has largely washed out and the company is moving into the hands of value investors, as shown below using Factset holder style categorization:

After management’s catastrophic Q4 call, which included initial 2025 revenue guidance well below consensus (12% growth vs ~20% consensus) and a pricey, seemingly dilutive acquisition that consumed half their net cash hoard, we believe the market was left confused as a full-fledged Bear Case seemingly reared its head.

Whereas management was previously viewed positively, the size and explanation of a major acquisition at a time when the rest of the business was struggling, combined with a major Reduction in Force (RIF) made the market reflect on whether perhaps this team’s talents and capital allocation were not as good as originally thought. We believe the messaging was confusing to both value and growth-oriented investors. Managment was simultaneously telling investors that they were aggressively curtailing spending through the workforce reduction while also splurging on a large, expensive, dilutive acquisition.

Voss Variant View

Although we acknowledge these missteps, which we view as a combination of poor messaging and, honestly, some plain ole bad luck, we still believe the operational execution remains strong and have developed variant views on what we view as current short-sighted consensus perceptions, summarized below.

Consensus Perception vs Voss Variant View:

The TAM in Education is Saturated

We believe their remains sizeable opportunities to add new clients outside of the top four markets (US, Canada, Australia, UK) but more importantly, we believe they have several more years of strong growth in moving more customers to their Student Financial Services (SFS) platform. This narrative will begin to emerge in the coming quarters as they roll out SFS in the UK more aggressively.

Extreme Vulnerability to Macro/Regulatory Environment

We believe they have gone through close to the potential worst-case scenario, and that things are likely to get better in the next 2 years (or at least not actively worse), but absent that they are quickly diversifying, not only into other verticals, but becoming less dependent on first year international students driving growth through their SFS launches. Our variant view (perhaps) is that there is not some secular change in demand/supply for study abroad, but rather there are ebbs and flows, and we are nearing the end of an ebb.

US/China Tension Can Materially Disrupt the Education Business

We acknowledge the potential cooling of demand in the US market given political rhetoric but believe the “nuclear option” (e.g. banning students from China or putting harder caps in place), is unlikely. Further, breaking down the actual impact of this risk suggests it is highly manageable.

Low Student Retention

SFS launches, as well as more proactive education from Flywire to universities, will significantly help solve this problem, as we don’t believe Flywire is more expensive than a bank wire. There would also seem to be potential partnerships with banks or neobanks that could help improve retention.

Management Are Questionable Capital Allocators and the Sertifi Acquisition Showed Desperation

We believe there are tangible, significant revenue synergies in the Sertifi deal that should make the acquisition closer to their blockbuster WPM acquisition in the UK as compared to their less successful Simplee acquisition in healthcare. Depending on priorities, the B2B segment also seems ripe for significant further expansion.

Healthcare Was a Failure

We don’t completely disagree, but we do see significant acceleration from this business in the back half of the year, and believe management is actively considering pruning it from the portfolio to focus on Education/Travel/Hospitality.

The Flywire Education Business

Despite growth in their Travel and B2B businesses, Education remains about 75% of total Flywire revenues and thus is still the primary driver of the stock. We think the market remains confused about Flywire’s education business, both in how they make money and how they retain both universities (customers) and users (students), with myopic focus on first year enrollment in various regions. If we are right on our thesis, the market is even more confused about the trajectory and potential growth.

The roots of Flywire’s products, and to this day what many universities primarily use them for, are an avenue for international students to pay their tuition from their home country. Paying tuition outside of one’s home country is a different workflow than paying domestically, with the primary difference being the need to convert the payment from one currency to another and dealing with various regulations around capital outflow from the originating country. It may seem simple, but there is substantial value in being able to do this seamlessly, both to the university (primarily around reconciliation and security) and to the student/student’s parents (for useability and flexibility).

For instance, in China, India, and other countries where capital flight is a concern, there are restrictions on how much and under what circumstances citizens can send money out of the country. Flywire and a small number of other companies have relationships with China, India, and most other countries to act as a Payment Service Provider (PSP), similar to companies like Square, Paypal, and Adyen but focused on specific verticals. Because of these relationships, it is far easier for a parent in China to utilize Flywire to pay a tuition bill than it would be for them to wire it to a bank in the United States and pay it from there. For the university, the currency conversion messiness can often result in slight discrepancies in what is paid versus what is owed, which can then become an administrative headache tracking down those discrepancies and getting full payment. Flywire’s basic “light” product does all this quite well, but it’s limited to those payments and only those payments. Flywire generates revenue here essentially by currency "off-ramping", pocketing a small percentage of the transaction (we estimate ~1.75% take rate for currency on average) during the currency conversion, while also charging the universities an annual software license fee.

We believe Flywire’s initial “land grab” of growth in Education was defined by establishing footholds in universities across the world (with a focus on US/UK/Canada/Australia) with a product that worked quite well and solved a real problem but was a bit limited and was susceptible to churn on the user (student) side as the international student eventually set up bank accounts in the destination country. In fact, you could make a short case around Flywire’s net revenue retention (NRR) numbers being inflated as much of it was simply a product of landing in a university and capturing freshman students, then retaining enough sophomore students to show strong “retention”.

For example, College A adopts Flywire and most international freshmen students use it in year 1. Further, let’s say in year 2 a full 75% of the now sophomore students churn off Flywire and pay using some other mechanism as they have established domestic bank accounts. If Flywire captures a similar number of first year students, their net retention would show up as 125% (e.g. 100% of replacement freshmen students plus 25% of sophomores). However, this song and dance can only last 4 years and by the fifth year you no longer have a “new year” to add and reported retention would likely go down. In other words, 25% user retention can look like 125% university revenue retention for a few years, then fall off a cliff (closer to 100% unless they can improve student retention), simply by the mechanics of the four-year university cycle.

The real prize for Flywire is the “land and expand” strategy of getting universities to use Flywire as the exclusive or semi-exclusive “payment portal” for what they call Student Financial Services (SFS). In this case, Flywire becomes much more enmeshed in the university workflow as now virtually all tuition payments (both international and domestic) are processed through Flywire. Not only that, because of the strong two-way integration between Flywire and the university ERP, Flywire’s software is often used by administrative staff as it’s more user friendly and intuitive than the ERP.

Landing an SFS contract results in multiples of revenue at the university, as previously Flywire might have been processing 10% of payments and with the adoption of SFS they process nearly 100%. However, a 10% to 100% jump is not as simple as a 10x revenue jump because processing domestic payments carries lower take rates than if the payment involves a currency conversion (they do not disclose this rate, but we estimate 1/3 the rate or less). The real one-two punch is if Flywire can simultaneously get the university to use their SFS product while also increasing the percentage of currency conversion transactions.

The SFS (R)evolution: Cracking the UK

In the UK, we believe Flywire has developed a unique template that not only provides a great value proposition for universities to use SFS but also encourages international students to “leave their currency at home” when paying through Flywire, maximizing both total payment volumes processed (~100% of students) while also maximizing the value of each student (international students paying from home).

While the UK has already become Flywire’s largest education market from a revenue standpoint (per management), it's a core part of our thesis that Flywire is still in the early innings of seeing the real uplift from SFS, as they just completed the first of several major ERP integrations and are seeing preliminary (but significant) success in the UK that can drive full Student Financial Services (SFS) adoption and thus increase revenues at the university from 2-25x, depending on where the university is starting from and the breadth of solutions they take.

We think there are four things Flywire is emphasizing that are helping them land significant contracts in the UK:

They educate the school and show them that by students “leaving their currency at home” and paying through Flywire, it saves the university substantially on fees. If a student pays through Flywire internationally, the fee for the university is zero, whereas if the student pays locally (even through Flywire), there are transaction fees the university incurs.

By building real time integration with the school’s ERP (for example, Unit4, which is in 50+ major UK universities), there is a significant reduction in manual labor and adjustments that allows the university to use their administrative staff more effectively or potentially reduce staff. They just completed Unit4 integration in Q4 2024, and by Q1 announced signing four UK universities, with a large pipeline of at least 50 additional schools. We believe some of the “macro pressures” could help accelerate adoption here as schools are looking to save money.

By using Flywire’s Collections Management System (CMS) software and Payables software, the university can save materially on paying collectors while receiving a 3x uplift on unpaid tuition recoveries, as well as receive lower rates on Payables fees compared to what banks offer.

Provide a profit share with the university upon certain retention thresholds.

We believe the first two items are most important as per our discussions with people on the ground in the UK, convincing and marketing students to “leave their currency at home” can save the university a substantial amount of money (hundreds of thousands for a large university). Here is a Manchester Metropolitan University Finance Head, one of a handful of SFS beta customers, describing the benefits they experienced by directing students to “pay from their home country”:

“The reason why it’s game-changing is because all those universities that still, in the main, encourage students to transfer the money to a UK bank account so they can collect in sterling don’t have to do this anymore. They can tell students to keep the money in their home country because this SFS product will engage them at the front end of the cycle…not only will you not have to pay anything for that transaction, but you’ll save about £200,000 (GBP) in transaction and acquirer fees because you’re no longer paying the bank charges, you’re no longer paying Visa or Mastercard, and you’re no longer paying handling fees. You’re no longer having to manage it yourself as an organization.”

The person quoted later clarified that the £200,000 (GBP) in savings was for around £20 million in processing, and that they process multiples of that, so they may ultimately save in the range of £800,000-£1 million pounds ($1.1-$1.3M USD) a year just in fees.

This individual further explained that by launching SFS with its seamless simplicity, they have cut down “student engagements” (e.g. calls/emails from students having issues paying and sorting their financial situation) by 90%:

“When we went live with Flywire’s SFS model in 2021, my finance team had engaged with students around 32,000 times…this year, and we’re pretty much towards the end of the academic year now, we’ve done 3,100 engagements. We’ve reduced our engagement since live with Flywire’s SFS model by 90%. That’s enabled us to refocus our staff in doing value-added stuff.”

Note this is the first of merely a handful of test sites, so they may have around 5% or less penetration with SFS for a market where they have 80%+ market share of international payments already. It is our understanding that there is no competitor that can even come close to matching this, specifically the intricate ERP integrations, and that the primary reason you won’t see all the schools just move to this is the generally glacial pace of change at bureaucratic UK universities administrations. Thus, we see an opportunity for the already sizeable UK business to become significantly bigger over the next 2-3 years.

You may be asking how the students feel about this. Is it a bit cheaper to move all your currency into a bank account in the UK and then pay the school rather than pay directly? We believe it might be slightly cheaper, but the degree of cheapness is a rounding error compared to the ease and flexibility of payment options that Flywire offers, and the slightly cheaper costs assumes you are not doing multiple transactions throughout the year. Using Flywire cuts the total number of transactions in half (e.g., move money into a bank which involves a currency charge, then pay domestically, which triggers other banking charges).

According to the people we have spoken to, the students embrace it because of the significant flexibility of choice in how to pay (e.g. Alipay, ApplePay), the breadth of currencies offered, and the slick flexibility in providing payment options (e.g. set up daily/weekly/monthly plans, pay from your bed, allow parents/sponsors/relatives to pay directly from the home country). Here is how it was framed to us in various snippets:

“I once got a load of Chinese students in a room and I said, ‘I need to understand something from you because you’ve all made payments through Flywire in the last six months, but you’ve not all chosen the cheapest Fx rate. I need to understand why you’re not choosing the cheapest Fx rate…this Chinese student got up and he said, ‘I’m speaking on behalf of all students who are in this room…it’s not for you to tell us what payment option I choose. It’s for you to give us the choice because you don’t know what kickbacks I’ve got in my country. You don’t know what financial incentives I’ve got by having that particular payment…you’ve done what we asked you for, and that is provide choice. Payment choice is what we want.’”

“We now have 94% uptake, so that is if you joined last year, we’ve still got 94% of students that are paying in [their home] currency in this year.”

In other words, by making Flywire a flywheel, it mutually benefits Flywire, the university, and the student as well.

Doing the math on this, we believe just moving 20-25 universities over to the SFS system in the next couple of years would grow UK revenues by $50M+, or over 50%. Could the uptake be even higher over the next couple of years? Well, the person we talked to was so excited about how his product was working for him, he is now presenting his experience (for free) to other universities on behalf of Flywire:

“I am being asked to present two universities a month at the moment, minimum. Actively, I have a project manager that works alongside me, and we are both happy to engage universities. We have a standard presentation that we deliver to universities. Almost every single time we present the FD or the CFO turned around and said, ‘That’s exactly what we were told by Flywire, but we needed to hear from a university’.”

For an industry that is generally reticent to change and particularly swayed by others’ experience, this is powerful to have an advocate running around making presentations on behalf of Flywire. Word of mouth will fuel the pipeline and help close deals, and we are quite optimistic about the opportunity set here, not only in the UK, but the potential to follow this same playbook across the rest of Europe as more ERP systems are fully integrated. Management cautioned us that the rest of Europe would likely not start this year, but partly this was because they “still have so much opportunity in the UK and want to make sure we get it right in other markets.”

Some of the company’s early SFS learnings in the UK can also be applied to the United States, specifically getting the school to actively market international students to pay remotely. While the United States is clearly more competitive, our conversations indicate strong satisfaction with Flywire while other vendors have more of a lukewarm reception. For instance, here is what a director at Stanford said about Flywire relative to the competition:

“I would say 90% of our payments and also bank transfers [go through Flywire]. We have a bank wire, and we’ve made a concentrated effort to move our students away from the bank wire and over to Flywire. Ultimately, we want all of our international payments to go through Flywire...I think that (competitor) Convera is a great option. I feel like just from experience and use with Flywire, Flywire is more seasoned. Their system, their platform, their service and also options for the students as far as the conversion options are more robust with Flywire than Convera. It’s just an overall easier process, it seems, for our students using Flywire. We have tried to market, you would say, Convera more, but the preference tends to be with Flywire.”

To summarize, we believe the narrative around Flywire hitting some kind of wall in education is very misguided and the fear is overblown. Even in their largest and “most penetrated” market of the UK, we believe there is a real opportunity to at least double their revenue base over the next few years. Many other markets with weak competition remain mostly untapped, while learnings from the UK can help growth in the largest potential market, the United States.

Potential Macro/Regulatory Pressures in the US and UK

Although we attempted to articulate that first year enrollments for students should play less of an issue for Flywire (because of diversification within education and the burgeoning Travel vertical), we can understand how investors are weary of additional issues after Canada caused such unanticipated disruption for the company, and now both Canada and Australia appear to be headwinds again in 2025. The concern is that the next “shoe to drop” is the United States or United Kingdom (or both), the biggest two markets for Flywire.

While we cannot eliminate this concern in the medium to long term, we do not yet see material signs of this being an issue in 2025, outside of some likely declines in the US market that in the context of guidance feels very manageable to us.

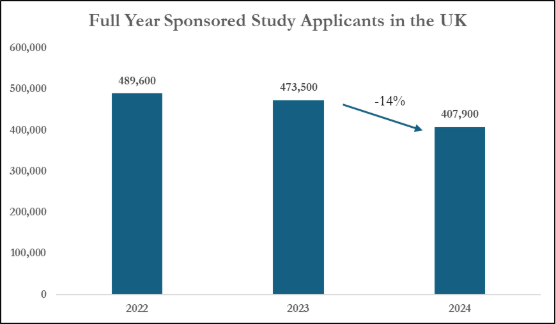

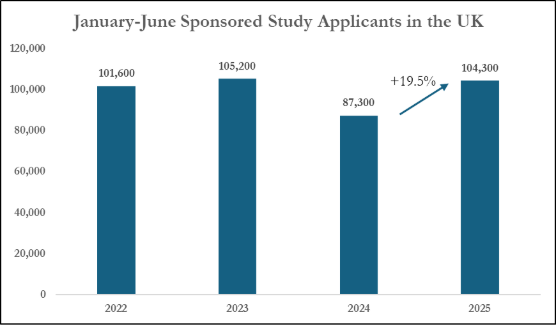

Looking at the UK first, it is true that the government has done some things to make studying abroad less desirable. Starting in 2024, the government no longer allowed family members to accompany students with them to the UK. This did appear to have an impact on total visa applications, as shown below:

While we don’t have exact UK revenue data for Flywire from 2023-2024, it’s pretty clear this decline in visas in 2024 did not slow Flywire’s UK growth down. In fact, it’s possible that by parents not coming with their child, it potentially increases currency conversion payments despite fewer total students.

Looking at 2025, while it is true July-September is where most student visas applications occur, thus far through June we have seen a near 20% rise in UK visa applications, with numbers bouncing back to 2022-2023 levels.

Management noted that their working assumption embedded within 2025 guidance is that the UK would have a similar drop as from 2023-2024, so things would really have to fall apart at this point to reach that level.

The reason this was the original guidance assumption was that the UK government was working on other specific items that could limit total visas. If we look at the original document from the government document titled “Restoring Control over the Immigration System- Technical Annex”, it outlines (with estimates) how it could impact total international students, with the potential changes impacting around 37,000 students when adding up the various components of the recommendations. This would be around 9% of visas at the current run-rate. We would note, however, that these are merely proposals and the only guideline implemented (increased skill level requirements) would have an estimated impact of only 9,000-14,000 students.

There are other early positive anecdotal data points. We recently broached this subject with a Director of Finance at the University of the Arts (in London), and he expected similar international enrollment this year as last year, emphasizing they were spending aggressively to market and work with international students because of how valuable they are:

“It’ll be relatively similar [this year versus last] ...the challenge here isn’t the fact that we don’t want UK students. That’s not actually the challenge. It’s because of the payment. Remember, we are forced to charge less than £10,000 (for domestic students). We don’t have a choice...our international students, they are actually subsidizing our domestic students.”

We think this is a key point. Universities are not just ambivalent about replacing a domestic student with an international student--they need international students to attend their university and will likely spend money on recruiting to drive international enrollments. This sentiment was reiterated recently by Unite Group, a REIT in the UK that focuses on student housing. On July 8th this group noted that “student numbers are expected to increase for the 2025/2026 academic year due to improving trends in international student recruitment.”

Finally, there is a UK application called UCAS that puts out periodic summaries of acceptances which indicate that, through June, accepted international undergraduates were up 4% y/y.

Between these anecdotes and the run-rate data showing between 4 and 20% growth, combined with management setting a low bar in guidance, we feel reasonably confident in the UK setup.

United States Education Market

In the United States, it is admittedly harder to get a good read on trends, and we do think there is real risk that visas come in lower in 2025 than in 2024, perhaps materially so. For instance, a recent report from the International Institue of Education (IIE) suggests a higher percentage of schools expecting a decline in international students (albeit 32% still expect an increase and another 32% still expect “stable”). However, the “nightmare scenario” that started to emerge when the Trump administration was aggressively posturing to both China and major universities around their enrollment practices seems to have died down. In late May, there was a “temporary pause” on new visa interviews. As we understand it, this pause ended in late June, lasting less than a month, and was framed more as updating their social media criteria vetting process rather than any stance on restricting total visas.

Further, for the moment Trump seems to be OK with ongoing Chinese enrollments, tweeting out:

“WILL PROVIDE TO CHINA WHAT WAS AGREED TO, INCLUDING CHINESE STUDENTS USING OUR COLLEGES AND UNIVERSITIES (WHICH HAS ALWAYS BEEN GOOD WITH ME!)”

Yet given Trump’s long history of quickly reversing positions when it is expedient, we certainly cannot rule out a risk starting in 2026 that visas are limited more broadly or targeted at specific countries. It is our view that the most likely longer-term risk is that tensions escalate further with China. The shorter-term risk is that the rhetoric has a cooling on demand to study in the United States that the universities do not have time to counteract that in the 2025 recruitment period. Given the pause in interviews during most of June, we do expect miserable June visa estimates but would expect things to begin picking up substantially in July/August. Walking through the numbers with the CFO, this is how it was framed to us:

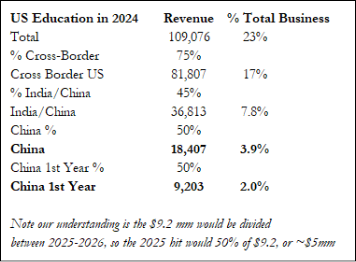

First, if we look at the entire US cross-border revenues, it’s about 15.5% of proforma revenues when including Sertifi ($82M versus $520M total proforma revenue). We believe roughly half of that is first year students, so around $41M. Hypothetically, if there was a 25% drop in first year enrollment, which seems very high but possible to us, we are talking about a revenue hit of roughly $10 million (2%) that would have to be made up in order for the company to achieve their “low single digit US growth” embedded within guidance. It seems plausible to us that this growth could be made up through a combination of SFS signings (5 in Q1 in the United States), new university signings (nearly 800 new customers announced last twelve months, although the total within US education is not known), and/or general retention initiatives between grade levels and across grad programs.

Or we can assume a more targeted hostility to China. Losing all first-year Chinese student revenues would be contained to a mere 2% drag on total FLYW revenues. If all Chinese students were banned at once (which would imply to us some kind of military confrontation with China), there would be a ~4% hit to revenues. Still manageable.

We also believe that students who bail out on studying in the US this year would likely apply and attend school elsewhere, as this is not a country-of-origin supply problem. The IIE report stated that “nearly three-quarters (71%) of U.S. institutions noted that prospective students may be choosing to enroll at universities outside the United States.” In this case, the NET impact to Flywire would likely be smaller as Flywire has a strong presence across the globe, and the likely alternatives (UK, Australia, Canada, and continental Europe) are areas of particular Flywire strength.

Having said that, we do view the degree of US enrollment decline as the biggest risk and unknown to our thesis as it is hard to quantify. We believe the bar has already been set very low and the actual impact is manageable as described above, but we cannot rule out either greater short term demand destruction than we are anticipating, new headlines, and/or policies that could threaten the long term health of the study abroad ecosystem in the United States. Given how important international students are to most United States university’s bottom line and in some cases sustainability, we would expect a rebound next year with more aggressive recruitment tactics to entice students to come (like what we are seeing in the UK), combined with aggressive lobbying on the political front.

Riches in Niches: Exotic Travel/B2B Travel and the Sertifi Acquisition

Flywire has historically focused on niches that involve larger, more complex payments across countries, and their push into Travel and B2B fits neatly into that framework. The growth here, which has been organic up until Sertifi, is impressive:

Note from their disclosures we believe Travel is about $60M while B2B is about $15M. The company is trying to position the Travel vertical’s success and potential as like Education, showing the “first five years” of each cohort, with Travel (allegedly) eclipsing Education in gross profit dollars by year 5:

When Flywire announced they were acquiring Sertifi, the timing and size of the acquisition was optically about as bad as it could get. Flywire, even prior to their collapse from $18 to $9, trading at around 3x sales, buying a Sertifi business that they claimed would add “$30-$40 million in revenues” for around $350 million. So, a 3x sales business buying a business at 10x forward sales while using more than half of their cash, right at the moment you announce a material RIF and lower guidance for the underlying business. Oof.

Given the vague guidance on EBITDA contribution from Sertifi, we were also left to wonder if this acquisition would burn additional cash. We estimate that the acquisition, given its size as a percentage of total enterprise value and minimal expected EBITDA contributions, increased the underlying EBITDA multiple of the stock by 2.5x turns, which significantly lowered the potential floor of the stock if an investor is trying to put a line in the sand on EBITDA multiples. In other words, if 8x EBITDA was our previous Bear Case floor, this acquisition just forced us to lower the Bear Case target substantially (this quarter was just bad news for both Value and Growth investors).

We also think the company did not do the best job on the initial conference call articulating the potential upside and value proposition, resulting in effective panic selling as regulatory clouds seemed to get darker and the value investors were ascribing to their cash hoard was lowered.

All that said, virtually every new piece of information we have learned about this acquisition since the announcement has put it in a much more flattering light. We still believe the cost was high and think the timing and communication was poor but now see a real possibility that this asset can drive material revenue synergies while also continuing to expand the TAM into natural adjacencies.

The first thing to know is that the $30-$40M of revenue was not Sertifi’s total revenue, but 10 months of revenue. Thus, instead of $35M in revenue we were actually looking at $42M in revenue at the midpoint (proforma), and closer to $50M on the upper end of guidance, lowering the implied sales multiple somewhat. Second, Q1 results indicated that at least for that quarter, Sertifi was not going to be a material margin drag. In fact, Sertifi was accretive to margins in the quarter:

We do expect Sertifi to be a modest drag on company margins as the company makes some investments and we get to the seasonally higher margin quarters of Flywire’s core business, but this was still much better than we were originally expecting.

More importantly, conversations we have had with hotel industry players suggest to us that not only is Sertifi a well-entrenched, high-quality, fast-growing SaaS asset in the enterprise hotel space, but the revenue synergies are straightforward and appear to have preliminary support from some of the largest chains using it like Hilton and Marriot.

A Hilton person we talked to was already intimately familiar with both Sertifi and Flywire functionality and explained how Flywire’s features were highly complementary to Sertifi:

“A few examples are Sertifi doesn’t have multi-currency support today, so it charges in USD and therefore, you’re subject to your bank’s foreign exchange rate. Flywire has that capability, and it also has its own built-in foreign exchange. As I understand, it’s better rates than the banks offer so that’s a cool additional capability. The other thing that Flywire has, Sertifi doesn’t, it has local integration to a lot of the regional payment processors so it just allows more extensive integration from a global perspective. You can do payment plans with Flywire, you can’t do that with Sertifi, and you can do split payments with Flywire, which you can’t do with Serfii…when I think of the integration and acquisition, I get excited about the payments aspects.”

In other words, Sertifi is strong on contract workflows (essentially a Docusign for hotels, with superior Property Management System integration) but is missing some specific payment functionality (especially for currency), which is precisely where Flywire thrives.

This person claimed “at least” 50% of Hiltons are using Sertifi, but this was strongly tilted to their American hotels where currency conversion was less necessary, so he also thought the acquisition would be a way to get Sertifi onto the rest of Hilton’s hotels:

“Just leveraging different currencies and that capability is going to make Sertifi a lot more attractive to our hotels internationally…Sertifi does not have much penetration in our APAC market…it’s good for us internally from a system perspective too because the more payments we get going through Sertifi, that means fewer payments going through the one-off integration or non-standard methods that we’ve set up. It streamlines processing on our side which reduces cost.”

To us, this is an explicit and unusually strong endorsement of an acquisition by a large enterprise customer. Although we would not expect Hilton to immediately adopt Flywire in all their hotels as it sounds like some integration between Sertifi and Flywire needs to occur, the 2–3-year opportunity seems to validate management’s rationale for doing the deal and perhaps paying a bit more than they might otherwise would have. Management has talked about how layering on payments with a Sertifi customer can increase revenues for Flywire “by multiples”, so they don’t need to cross-sell that many hotels on Flywire payments before the math of the acquisition starts to work.

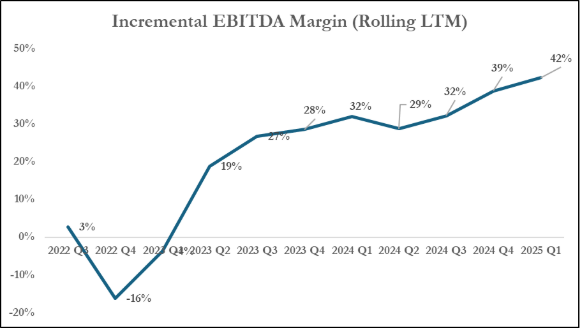

Flywire’s Emerging Profitability

A criticism of Flywire coming out of the gate was their poor profitability. In fact, through 2022 they were still running at a negative incremental EBITDA margin. Since then, though, their incremental EBITDA margin has skyrocketed to above 40%, as shown below:

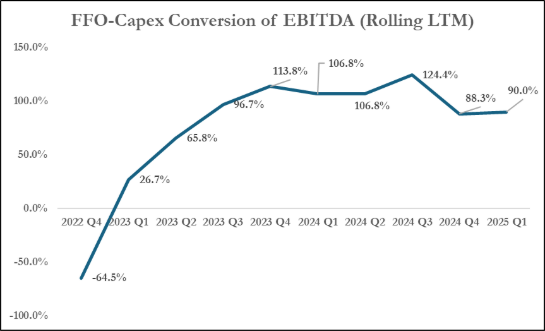

Because the company has significant net cash (e.g., positive interest income), very low capex (~1% of sales), and is a low taxpayer, their underlying FCF conversion is quite strong as well.

It is true their working capital is volatile (primarily because of “Funds Payable to Clients” and “Funds Receivable from Payment Partners”), so we believe looking at Funds from Operations (FFO)–Capex is a better gauge of underlying FCF. Looking at this metric, Flywire has converted at or around 100% of EBITDA:

While the Sertifi acquisition may hit these metrics modestly in the short term, and we would note that some of their Travel revenues come in at lower gross margins (which could modestly slow down additional gains in incremental EBITDA margins), we see no reason why the company cannot continue to run near 35-40% incremental EBITDA margins and 80-90% FCF conversion.

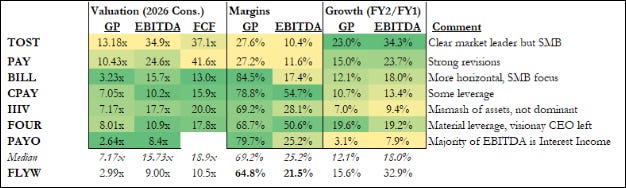

Trading Comps

At the risk of alienating people, we will compare Toast (~15x NTM consensus gross profit) to Flywire (3x). Before going further, we believe Toast should trade at a premium to Flywire because of their excellent, more consistent organic execution, still stronger growth profile at a larger scale, and likely larger more immediately addressable TAM.

However, we’d like to point out that the two companies really aren’t that different and, if Flywire had had just a neutral macro/regulatory environment the past year or so (as opposed to a nightmarish one), their growth profiles might look about the same. Moreover, we think Flywire’s customer base is almost certainly sturdier than Toast’s.

Toast is a technology company in the restaurant industry that leads with a strong software platform but monetizes primarily through payment processing.

Flywire is a technology company in the education and hospitality industries that leads with a strong software platform but monetizes primarily through payment processing.

Toast can be characterized as dominating in US SMB restaurants, with some fledgling but unproven success with larger restaurant chains and emerging potential with international restaurants, while also continuing to monetize their existing customer base.

Flywire can be characterized as dominating cross-border tuition payments around the globe, with emerging but still somewhat unproven success in capturing the larger education payment workflow through their Student Financial Services products and growing success in extending their technology platform to other verticals, namely travel and hospitality.

On the positive side of the ledger for Toast, their entrenched position with point of sales (POS), the “brain” of the tech stack, makes their offering more mission critical than Flywire. You could also argue Toast is working with a larger (more immediately addressable) TAM, although we would argue Flywire has numerous emerging opportunities with gigantic TAMs (like B2B payments).

Flywire has some relatively positive characteristics as well, though. For instance, Toast’s reliance on “mom and pop” and small chain restaurants means they will constantly have to spend some percentage of revenue on Sales & Marketing just to offset chunks of natural churn of restaurants going out of business (some estimates are that 60% of new restaurants fail within three years). Flywire is clearly more “enterprise” focused, with established universities, hospitals, and global hotel chains that lack the existential risk that one-off restaurants have. Further, Toast’s cyclicality is also underscored by payments levels dropping, directly impacting revenues, whereas Flywire's education business is counter cyclical. Finally, while acknowledging both companies have some regulatory risk on their payments “take rates”, we would also point out that Toast, which clearly charges smaller restaurants way more than what larger restaurant chains negotiate, could more easily come into the crosshairs of regulators looking to level the playing field.

We are homing in on Toast primarily because there simply are not that many good comps for Flywire. A lot of other transaction comps are more horizontal or SMB/consumer focused (e.g. Block, Global Payments, Bill.com), much more levered (Shift4, Global Payments) are smaller or unprofitable with no clear dominating vertical (i3, Lightspeed) or have radically different unit economics (e.g. Payoneer who generates a large % of EBITDA from interest income). Indeed, probably the next best comp was recently acquired (AvidXchange, see below).

Nevertheless, here is our comp group, using 2025 and 2026 consensus median estimates:

Transaction Comps

Corpay and TPG agreed to acquire AvidXchange (AVDX) for $10/share on May 6th for $2.2 billion dollars. One day after the announcement, AVDX announced their Q1 numbers, missing EBITDA and revenues (2.2% revenue growth and flat EBITDA) which resulted in lowered 2025-2027 numbers from consensus, with 2026 EBITDA estimates around $96-$106M, implying a deal price of ~19x EBITDA.

Thus, this transaction valued AVDX at close to double the sales and EBITDA multiple of FLYW, for a company that just posted roughly flat EBITDA and revenue growth versus FLYW that is poised to grow EBITDA by over 30%.

We view AvidXchange as one of Flywire’s closest comps, as AvidXchange also has a similar mix of software and payments revenues and targets specific verticals like construction and real estate in processing B2B payables. Both companies are also of fairly comparable size, although Flywire is rapidly increasing their EBITDA and already has greater scale there. For the sake of conservatism, we use just 12x EBITDA in our base case for FLYW, a 37% discount to no-growth peer AVDX.

We would also point to Roper Technologies buying out Transact Campus in August 2024. Transact was projected to grow in the “high single digits.” They did have a 30%+ EBITDA margin but were purchased for 14x FY2 (2025) EBITDA including synergies with Roper's other education brand, CBORD. Although Transact did have a currency conversion tool launched in 2022, we believe Flywire is far ahead of it, with Flywire dominating other countries while Transact primarily operates in the United States.

Flywire as an Acquisition Candidate

Flywire has been repeatedly floated as an acquisition target, and for good reason in our opinion. In August, 2024, media reported that Flywire had been approached by suitors and had hired Qatalyst Partners to evaluate their options. Although apparently nothing came of these talks, Flywire strikes us as being potentially attractive to a number of industry players, ranging from strategics to private equity to software conglomerates like Roper.

Given Flywire’s strong access to and relationships with college students, we believe Flywire would be strategically interesting to any large bank (like say Capital One) or Neobank (e.g., Wise). In fact, we are surprised Flywire has not already partnered with banks and/or neobanks to drive retention. For instance, Flywire could refer their customers to a “preferred bank” who would help the student set up banking services so that the student could easily access spending money through Flywire. In fact, a former employee said a big reason they lose students after freshmen or sophomore year is the student needs outside funds anyway, and cannot use Flywire to achieve that, so they just go through a bank despite it being a giant hassle:

“Flywire only helps with tuition payments, but the student still needs money for the living expenses... A very big opportunity for Flywire will be to offer neobank capabilities like a wallet for students before they arrive to the US in a similar way to what TransferWise and Revolut companies are doing and capture those living expense flows. They’re looking into it, but they haven’t launched anything yet.”

We believe the synergies would be very obvious and that college students are viewed as high value marketing targets.

Additionally, with Flywire’s quickly burgeoning cash flow profile and strong balance sheet, private equity could easily LBO the company at 4-5x leverage and pay double the company’s current price while assuming only moderate growth levels (~12%) to achieve a 20% IRR.

Conclusion: Flywire’s Emerging Flywheel is Fixing to Flip the Faulty Narrative

Flywire is in a unique position of still aggressively adding customers in one emerging vertical (Travel/Hospitality), as noted by their ~200 new customers added in each of the last four quarters (off a base of 4,500 customers), while beginning in earnest the “expand” part of their “land and expand” strategy within Education. Thus, they still have strong customer growth while simultaneously showing burgeoning operating leverage through significant upselling and cross-selling. This is fairly unique in the space, as typically players are either in cross-sell/improve profitability mode, or are in cash-burn/aggressive customer acquisition mode.

We believe the market is not pricing in any of these positive dynamics and is instead agonizing over what “Trump might tweet next” or whether UK enrollments will be flat or down 5%. If you have a belief that there is a secular, global change in the attitude towards studying abroad (both supply and demand), Flywire is probably not the right investment for you. However, if you believe like we do that there are ebbs and flows in these dynamics, that the universities have huge incentives to retain and recruit as many international students as possible and that the value proposition of studying in the United States or the UK is still extremely strong, then you too can exploit the myopic short-termism going on in FLYW shares. In 12-18 months from now the stock could have a completely different narrative.

At 2x sales and near 10x 2026 FCF, Flywire is trading closer to the valuation of a company that is secularly declining versus one that is doing the disruption. In our Base Case, where investors develop a more neutral interpretation of their markets and competitive positioning, we believe the stock would move back to at least $18, representing around 5x EV/gross profit and 18x our 2026 FCF estimates. This multiple anticipates some reacceleration of growth in the back half of 2025 and into 2026. In a Bull Case, where the narrative flips closer to resemble that of a Toast or Paymentus, there would be materially more upside. In a Bear Case, where growth optionality does not pay off, regulatory issues continue, and the company focuses more on profitability, there is limited downside to around $9-10 (10x FCF on significantly reduced estimates).

Important disclaimers: https://www.vosscap.com/disclaimer

Thanks for sharing your work, which I found to be well written and high quality. Although American now, I'm from the UK originally and went to college there - I'd say that overall, the risk to the UK's international students is modest at worst. They just depend too much on the revenues those students bring, plus the UK is just way more diverse and has been for years and those students fit in well - contrast with the concentration of Punjabi Indians using student visas as a backdoor to PR in Canada. If there's one thing I'd love to see in the report it's just what your 2026 numbers look like as I have my own guesses. What jumps out in my numbers, even assuming continued pressure in the three troubled markets, is that the revenue mix has those three down to 15% or so in 2026 due to full year of Sertify and just good growth elsewhere and of course reduced revs from those markets over the last 2 years. It's just hard for these tails to keep wagging the overall Flywire dog. Hopefully the focus can shift to SFS grow out and also it would be great if they company is able to offer up some nuggets in terms of when and by how much they can augment the Sertify related revenues as I suspect they have a good sense by now and those numbers could be way more impactful on the positive side than the US may look on the negative. One potential acquirer to ponder as well - SOFI. They just did a $1.5bn common raise, and they service students of course so FLYW could be a good source of leads globally. Doubt FLYW sells themselves as their stock could 3x in a year quite easily (PAY went up 5x from the 2023 lows as their narrative changed for the better so it happens). Cheers

I was intrigued by your comments regarding the possible divestiture of the healthcare unit - so far the results from the operational review have been more run of the mill type stuff but such a divestiture could be stock price enhancing given how undervalued it is. Healthcare is the most standalone unit that doesn’t benefit from Flywire's global payment platform. The core of the unit was bought in 2020, coincident with a $120m funding round although not sure what they actually paid. As we now know, within the last year they have regained momentum with the business about to expand around 30-35% starting in late 2025 with the onboarding of the prestigious and large ("8 figure") NYC based hospital system. That reputation enhancing contract win is helping them develop the pipeline and it makes this unit very attractive as it could lead to a few years of good growth. I peg 2026 unit revs at $41m, and it’s a high quality recurring revenue stream. One healthtech payments firm I see is Waystar and it trades at 6.2x ev/sales on 2026 per consensus extracted from Koyfin. Stock seems like it's a low double digit grower so seems like a decent comp although I'm open to debate on this as I'm not familiar with it. That would peg the value of Flywire's unit at about $250m. Along with their $171m current net cash at 1Q25 plus maybe $100m NTM cash generation that's a lot of buyback firepower for a $1.3bn mkt cap. 40% of market cap to be precise. The whole firm trades at 1.6x ev/sales right now per Koyfin so offloading this asset (only 6% or so or 2026 revenues) at 6.2x, or even 4.2x) would go some way to offsetting the poor sentiment over the Sertify price paid (albeit the bulls on the stock will argue that like WPM in the UK, Sertify is a saas asset that's ripe for rapid payments monetization - and geographic expansion in this case as well). Crazy that this market is fixated on maybe a 2% risk to revenues from US cross border education when there's so much upside to numbers from other sources. Hopefully they stop taking the BS from the market and spell things out that these dummies can understand.