Garage Sale

A Hidden Play on Commercial Construction and Home Improvement With 150% Upside

As we have been sharing our research on US residential real estate, a few of our investors have mistakenly interpreted this as us going all in on homebuilding stocks. In actuality, home builders represent a relatively small part of a larger housing and construction themed basket within our portfolio. This basket is also comprised of building product and home improvement related businesses. One of these companies is Griffon Corp. (GFF). Many of you will be familiar with Griffon as we recently engaged with the company and won a proxy contest with nearly 90% of the non-insider shareholder votes earlier this year, resulting in a new independent director as well a declassification of the Board. This means there will now be nine directors up for election at the next shareholder meeting and all fourteen directors will stand for election at the 2024 meeting.

Griffon is a mini conglomerate with a hidden gem asset that we think may finally be on the path to realizing value for its shareholders. For years, Griffon has existed as an inefficient conglomerate with three unrelated business lines: Consumer, Home & Building Products, and Defense Electronics. In April, the company announced it had reached an agreement to sell the Defense Electronics business for $330 million or $300 million in after-tax cash proceeds or $5.62/share.

GFF currently trades at $23.00 per share with a market cap of $1.2 billion. With $1.5 billion in net debt pro forma for the cash from the Defense Electronics segment sale, GFF has an enterprise value of $2.7 billion.

The Consumer business consists of a collection of brands that manufacture and sell long-handled tools like shovels and rakes to consumers and professionals, as well as the recently acquired Hunter ceiling fan business. The Consumer segment will likely do $1.5 billion in revenue and $170 million in EBITDA (12% margins) in FY 2023 (ending September). While Consumer is a solid business and likely worth $1.2 - $1.5 billion itself, today we want to highlight what we believe is Griffon’s “hidden gem” asset and prime buyout candidate, the Home and Building Products business.

Home and Building Products

The Home and Building Products business is the largest garage door manufacturing business in North America and serves both the residential and commercial end markets through two brands - Clopay and CornellCookson. The business is fully independent from the rest of Griffon with its own management team and headquarters and, as we understand it, full finance, tax, and legal teams. Thus, the reported segment earnings aren’t just a segment contribution figure that is supported by a ton of additional costs at the Griffon corporate level but is instead approximately equivalent to the earnings of the business if it were fully standalone.

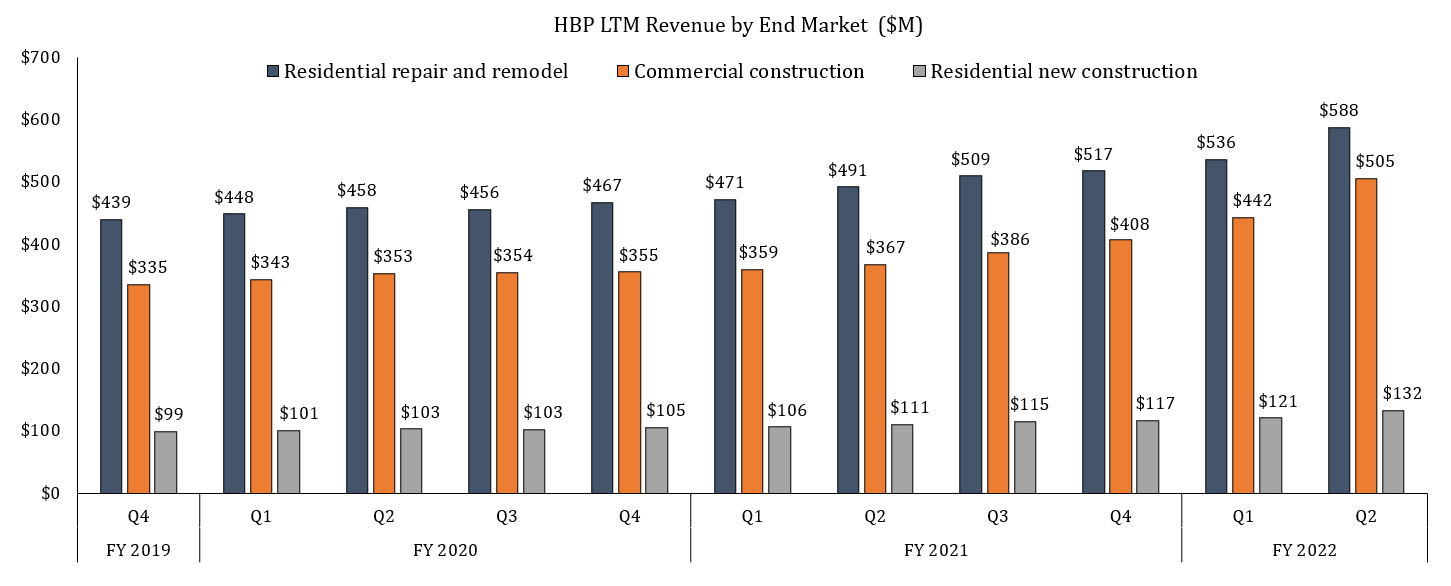

HPB’s revenue by end market is as follows:

48% - residential repair and remodel

41% - commercial

11% - residential new construction

We view this as a favorable revenue mix for a few reasons. First, residential repair and remodel spend is significantly less volatile than new home construction. Second, replacement garage doors carry far higher prices and margins than the typical low margin doors bought in bulk by home builders to outfit a neighborhood of tract homes. And finally, the commercial end market includes a range of building types from warehouses to retail stores to government buildings, along with a range of uses cases from security and thermal resistant doors, to climate control. This range of applications provides a much more diversified end market exposure and revenue base than something like pure new home construction.

Residential

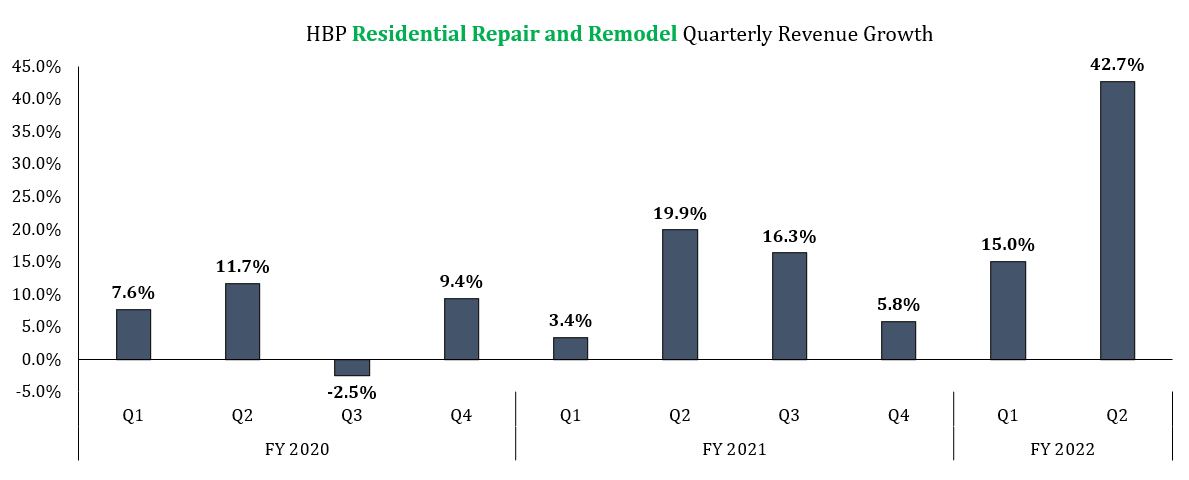

HBP’s Clopay brand leads the residential repair and remodel market with an estimated 30% market share of the residential market overall. The business weathered 2020 well with only a slight decline in revenue in Q3 2020. More recently, revenue growth has been in the double digits in four of the last five quarters including 43% for the three months ended March 2022. Price increases finally hit this last quarter and helped to further accelerate revenue growth.

From our channel checks, garage door prices are up anywhere from 60% - 100% versus recent years. The good thing about replacement garage doors is no one really knows what the average prices had been recently because they’re bought so infrequently. If a contractor quotes you $3,200 for a new door or $4,200 most people don’t have a frame a reference to know if that’s a typical price or not (current average is $4,000). Plus, relative to other home remodel projects that can easily run into the tens of thousands of dollars, garage doors are relatively inexpensive.

Unlike new homes sales and construction, home improvement spend is significantly less cyclical and not correlated with interest rates, with a statistically insignificant 0.15 R2 on a 14-month lag. Home improvement spend is instead driven by home price appreciation with a 0.52 R2 with no lag1. As of the end of 2021, U.S. home values and home equity were up 27% and 35%, respectively, since 2019. This bodes incredibly well for continued home improvement spend. If you’ve tried to book a contractor for a home remodel project recently, you’ll have noticed that most are booked out well into 2023 or are completely turning work down if the projected spend amount is less than six figures.

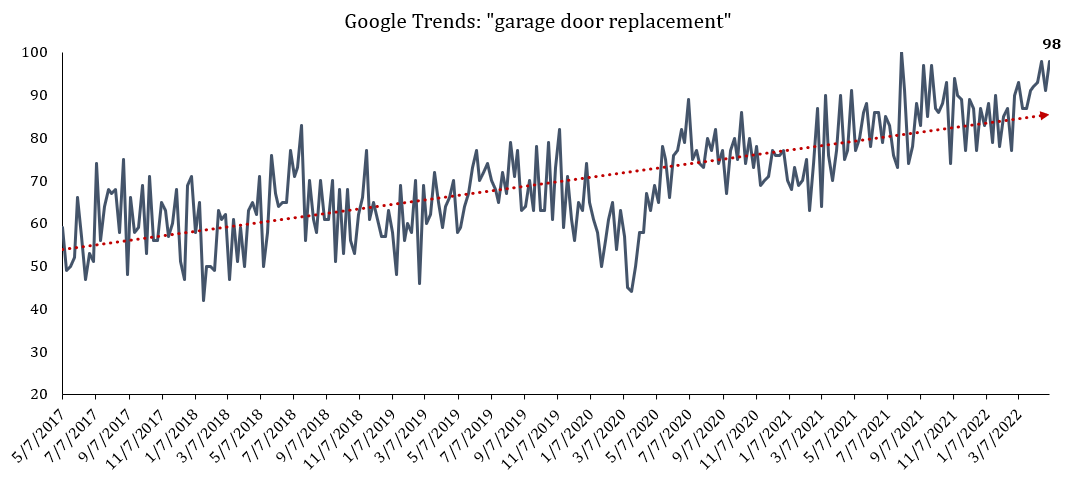

According to Remodeling Magazine, replacing a home’s garage door(s) ranks as the highest ROI project a homeowner can do in 20222. This is the 3rd time in four years that garage door replacement ranked the #1 ROI home improvement project. Given this, it’s not a surprise that Google searches for “garage door replacement” have trended up and are currently near an all-time high, a positive forward indicator for HBP.

Commercial

HBP’s CornellCookson brand similarly dominates its space as the largest rolling steel door manufacturer in North America with ~40% market share and is the “undisputed leader” in the industry according to a competitor we spoke with. Commercial sales held up well in 2020, never declining, and they have been accelerating for six quarters now including 66% growth last quarter with no signs of slowing down that we can see. Griffon says the backlog is currently “significantly greater than historical levels.”

Third-party leading indicators point not only to continued strength but an acceleration in commercial construction activity. The Architectural Billings Index is a 9 – 12-month leading indicator for commercial construction projects. ABI scores accelerated in March with a Billings score of 58, up from 51 in February, and Design Contract score of 60.5, up from 55.2 in February (anything over 50 signals an increase in work). ABI stated, “Indicators of future work strengthened this month… firms’ backlogs stood at an average of 7.2 months. This was an increase of more a month from one year ago and a new all-time high since we began collecting data on backlogs in 2010.”3

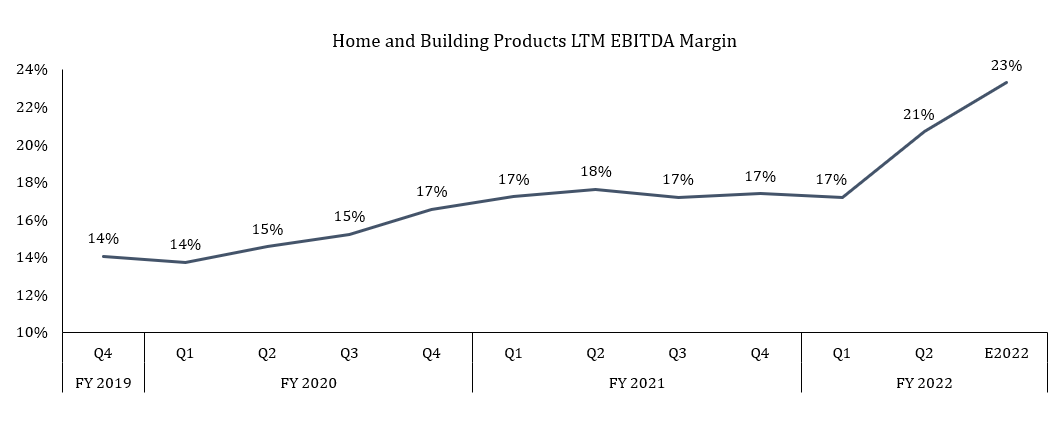

HBP’s margins have now reached >20% despite rising steel costs and supply chain issues, a level which competitors in the industry have told us should be a normalized level for HBP. LTM margins as of Q2 2022 were 21% with the company guiding for margins in the second half of 2022 equal to the first half (23%).

Given the revenue growth (despite continued supply chain issues) and margin improvement, we believe the company may finally be beginning to achieve its true earnings potential. EBITDA for the last 12 months was $253 million with the company’s recent increased guidance implying ~$330 million for the fiscal year ended September 2022. The business is highly cash generative with relatively low capex requirements. Since 2015, capex has averaged just $13 million per year and ranged from $8 to $23 million on a rolling LTM basis.

HBP is the type of business private equity should be snatching up right now. Over the past few years there have been a host of acquisitions in the building product space and specifically the garage door industry. These acquisitions have ranged from 11-15x, averaging 12.8x EBITDA. Given its growth prospects, leading market share position, high cash generation, and likely room for operational improvements, we see no reason why HBP wouldn’t also garner 12x. However, given the current valuation disconnect in the public market thanks to GFF’s inefficient conglomerate structure, we wouldn’t be surprised to see a buyer try to steal it for closer to 10x.

9x – 12x EV/EBITDA would value HBP at $3 - $4 billion, net of estimated taxes from a sale. To put this in perspective, Griffon’s current enterprise value is $2.7 billion at a stock price of $23/share. And remember, there is still the entire Consumer business doing $1.5 billion in revenue and $180 million in EBITDA likely worth an additional $1.2 - $1.5 billion. Taken altogether, we think GFF’s stock could have 150% upside to $60/share should the sum of the parts/conglomerate discount be unlocked.

Disclaimer: https://www.vosscap.com/disclaimer

Morgan Stanley Research - How Interest Rates May Impact Home Improvement Demand, April 11th, 2022