The State of Software

Is Profitability the New Growth?

Software multiples have collapsed from record highs over the last 5-6 months, going from a median of nearly 9.0x revenue in August 2021 to under 5.0x today. The average software stock has seen their revenue multiple nearly cut in half.

The common perception here is that the so called "high-flier" stocks which were trading at obscene 30x+ sales multiples a few months ago were in their own little bubble that is bursting and thus have borne the brunt of the severe deratings. The thinking goes that these high-fliers are primarily high growth and currently low margin companies, with most of their value deriving from cash flow several years out. As interest rates rise and investors put a higher discount rate on cash flows in out years then that value should get disproportionately hit relative to the lower growth, lower multiple names that are generating FCF right now.

We wanted to look at the history of software multiples as well as go under the covers of the software decline to answer the following questions:

1) Has anything outside of interest rate expectations changed at a fundamental level to justify the massive sell off?

2) Are the highest multiple names really bearing the brunt of the deratings and has "value" software mean reverted?

3) Have the low growth, higher margin names started to outperform high growth, lower margin names?

RingCentral

Not to pick on any one name, but we'll start by using an example to illustrate the severity of derating despite seemingly intact fundamentals. If we look at RingCentral (RNG), we can see that at the beginning of 2021 it was trading at 27x NTM revenue, with expected growth for the year around 25%. Fast forward to today, and the company’s expected revenue growth has rarely been higher (~26%), but the multiple has de-rated a full 80% from peak. One can certainly say this is an extreme case and there are likely other idiosyncratic factors (large growth funds concentrating into it and concerns about Microsoft/Zoom disruption), but we thought it would be prudent to at least show a representative illustration for what is a decided trend in the industry.

The Relationship Between Revenue Growth and Revenue Multiple

As you can see below, the median EV/Revenue for software companies is reasonably correlated with the median expected revenue growth (NTM/LTM). The derating has been intense, from 8.8x to 4.7x, but expected revenue growth continues to accelerate, now at 21%, a 20-year high.

Additionally, you can see gross margins remain remarkably steady over time within a range of 69%-75% so this is unlikely to have cause the de-rating.

However, EBITDA margins have steadily declined over time.

If we look at the “Rule of 40” over time (EBITDA margin + revenue growth), the metric is in a decidedly normal range.

For years, investors had been signaling that revenue growth was more important than EBITDA margin in the Rule of 40 equation. However, the current market environment suggests a reversal of this trend. Given that the EV/Revenue multiples have collapsed while the expected growth rate is the highest ever and the Rule of 40 is flat, it implies that investors have begun to exhibit more of a preference for profitability.

Will sustained, elevated interest rates make this shift in preference permanent? Or is the market perhaps signaling that the projected revenue growth and/or long-term margin targets are unrealistic?

Of additional interest is how various management companies react to this signal. Will they pull back on the cash burning/growth at any cost strategy (similar to how the E&P space has shifted to capital return over production growth)? Will there be a more balanced approach to growth and profitability?

At Voss we generally prefer a more balanced approach for our software stocks. If a stock is trading at 15x sales and burning a lot of cash to drive growth, it is hard as an analyst to estimate true unit economics and to underwrite a downside case. In situations like that, if you get the ultimate margin projections wrong the downside can be severe.

Are High Multiple Names Driving the Decline?

The short answer is yes, but with a caveat that ALL software is getting hammered from unusually high multiples.

"High-fliers" were historically valued at 4.5-7.0x sales until a massive breakout beginning around 2017. During this spectacular euphoria phase peaking in mid-2021, the group more than quadrupled their multiple to over 30x sales.

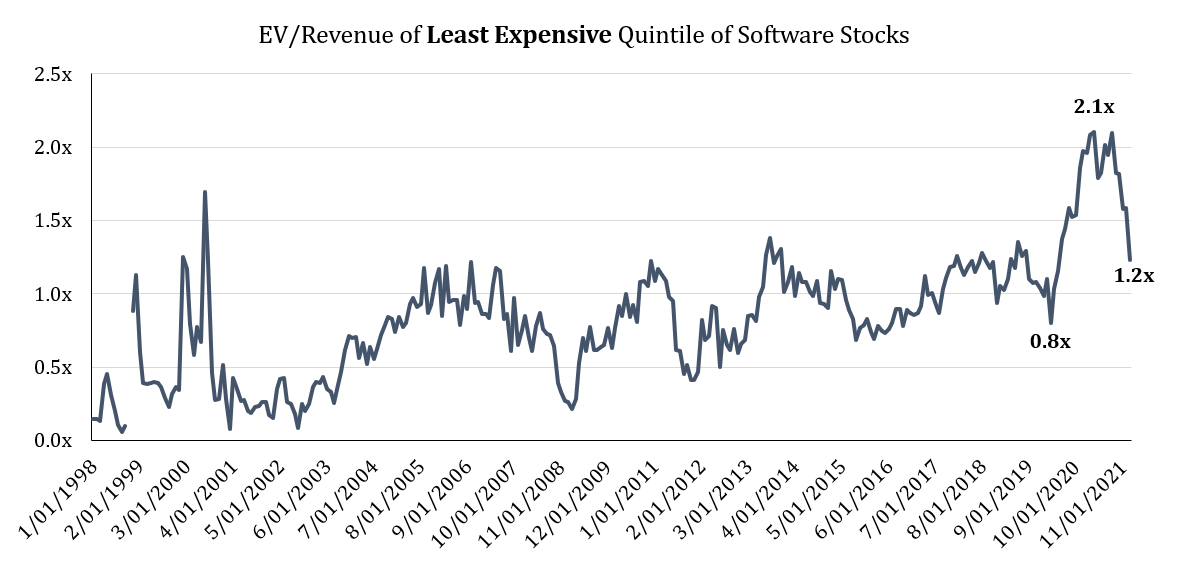

The cheapest software names also doubled their own historical multiple in 2020 and 2021 to over 2.0x sales.

Looking at the table below, the most expensive names have indeed led the derating, averaging a 58% decline from peak, while the cheapest have de-rated by 37%. So, while it is true that the higher fliers have led the decline, the tech stock crash has hardly spared the cheaper equities.

Another observation from the table below is that the most expensive names now have the *least* downside to their historical average revenue multiple, although there is still 24% downside as of mid-March. Remaining downside to historical averages is still 24-40% across the quintiles, so it is hard to say with any conviction that the software selloff is over.

From our point of view, the key to assessing whether there is further downside for software stocks is whether investors now believe potential margins could be higher than current/historical margins, thus these stocks will not necessarily revert back to historical average valuations. Or, equally plausible, the market is seeing that extraordinary capital inflows/competition are likely to cap terminal margins significantly below what some of the mature software giants enjoy today (e.g., Oracle/Microsoft). Perhaps it’s a little of both, and frankly it's an exciting time to be a stock picker as many companies may start to show their true colors, for better or worse.

Is Profitability Mattering More Now?

Finally, we wanted to see whether the profitability part of the Rule of 40 score was currently dominating, performance-wise. To test this, we divided the software space into two groups, one being high growth and low margin and the second being the opposite, low growth and high margin.

Looking at rolling relative 12-month performance, we see the following:

We can see that there was indeed a huge spike in 2020/2021 towards "growth at all costs." At its peak, while still not obtaining the even more ludicrous spread of >200% during the tech bubble, high growth/low margin software stocks outperformed low growth/high margin ones by 91% over a 12-month period.

Over the last 12 months this has materially reversed, as seems to be a pattern during corrections in the markets. To zoom in, here are the last 12 monthly spread returns:

Although there were some early rumblings early last year in March and May, the real hit to high growth/low margin came in November 2021 – January 2022. In those three months alone, higher margins/lower growth names outperformed their lower margin/higher growth peers by a cumulative 33%.

Conclusion

In our view, software as a maturing industry has proven it is stickier and less “disruptible” than perhaps previously thought. With the shift towards recurring revenue/subscription models, it's our belief that fundamentally higher multiples relative to the 1990s and 2000s are generally justified, as there is greater visibility and less volatility in financial results.

We suspect the massive relative outperformance by higher margin/lower growth software stocks is nearing an end and the returns will be more equal going forward, hopefully favoring names with a more balanced approach to profitability and growth, which has always been our preference.

It is possible that despite expected growth being at a 20-year and valuations having witnessed their biggest collapse since the tech bubble, there is still room for 20%+ downside. We can't rule that out. Many of the largest hedge funds have been concentrated in the same few software names so there could still be more de-grossing.

As we stuck to our valuation discipline, we had taken our software exposure from a peak of ~40% to start 2021 down to high single digit % and sidestepped most of the carnage. We now view software multiples as more fairly valued. If some high-quality software stocks decline another 20%, we might significantly increase our industry exposure once again as we would view it as an overcorrection for an otherwise healthy industry.

thoughtful note and perspective, thank you. can you please disclose what software universe you are using here? S&P 500? Russell 3000? something custom?

Wonder if the sell out is actually because it can also be argued that average base multiple should be higher now given all the tech focus and impetus has kicked in which is far higher than what is was pre covid?