Roaring Eighties

The Japanese Bubble during the 1980s

This overview of the Japanese Bubble during the 1980s is a precursor to our Inflation Investigation Series Part 2: Japan. It draws on notes from the book Devil Take the Hindmost by Edward Chancellor – Chapter 9, Kamikaze Capitalism, and Boom Bust by David Turner and William Quinn– Chapter 8, Blowing Bubbles for Political Purposes: Japan in the 1980s.

"The Japanese land and stock bubbles were purely political creations. Not only did the Japanese government provide the spark, but it systematically cultivated all three sides of the bubble triangle (marketability of assets, easy money/credit and speculation) with the explicit goal of generating a boom."1

The Bubble Lead Up: 1940s – 1970s

Most people are generally aware of the enormous Japanese asset bubble during the 1980s but we think it’s important to understand why a bubble developed in the first place. For that we must take a step back to the 1940s. Coming out of WWII, Japan’s prosperity was a key strategic interest for the US to show the superiority of capitalism, especially given Japan’s proximity to the growing communist powers. The US did what it could to help encourage economic development in the country and pushed reforms within Japan to match those of the US. One such example was the Japanese Securities and Exchange Law of 1948 which was modeled after the US Securities Acts of 1933 and 1934. The legislation significantly tightened securities trading and banned futures trading.

By 1955, Japan's GDP had recovered to its pre-WWII levels and then grew 144% during the 1960s. This economic success was largely driven by exports which leveraged Japan's world class manufacturing skills and competitive prices. To maintain this growth, the Japanese government fixed the yen to an artificially low exchange rate to ensure goods remained cheap for foreign consumers.

In the 1970s, the US began to push back on this practice under President Nixon and after ending the convertibility of USD into gold in 1971 most major currencies became relatively free float within a couple years including the yen. The yen appreciated from around ¥350 per $1 to ¥250, but relatively conservative fiscal policies in Japan kept the yen's appreciation limited beyond that.

The Plaza Accord

By 1980 Japan was thriving and now had comparable per capita income levels to the UK. The US continued to push back on the weak yen, and under pressure from President Reagan, the Japanese signed the Plaza Accord in September 1985. In doing so Japan agreed to increase the value of the yen relative to the USD by committing to three policies:

1. Vigorous deregulation to stimulate private sector growth

2. Loosen monetary policy and deregulate the financial markets

3. Reduce the government deficit

To offset the negative effect reduced government spending would have on GDP growth, the government strongly encouraged more consumer and mortgage lending. The Bank of Japan's discount rate dropped from 5% in 1985 to 2.5% in 1987 despite GDP growth exceeding 3% every year from 1981 – 1987. Cultural stigmas against borrowing money faded as household debt to GDP went from 52% in 1985 to 70% in 1990.

The restrictions put in place by the Securities Acts in the 1940s were gradually relaxed and the marketability of securities increased. Throughout history, the increased marketability of assets has proven to be a key factor to the formation of bubbles and this time was no exception.

The Bubble: 1980s

With rates low and regulations relaxed, the bubble only needed some fuel for the fire. This came in the form of excessive money printing with the money supply, as measured by M3, growing 141% from 1980 to 1990. Flush with cash and with interest rates unattractively low, investors began to pour their money into real estate in a newfound hunt for yield.

"For many Japanese, land ownership was still closely linked to social status, perhaps as a result of the country’s relatively recent feudal past. This was especially true for the older generation, who generally had the most money to invest. Since Japan was one of the world’s most densely populated countries, land also had scarcity value. Landholders were often very reluctant to sell at a loss, so the nominal price of land rarely fell, perpetuating the belief that it was an extremely safe asset."2

As a result of this “land grab” real estate prices in the six major Japanese cities would rise 4x during the decade.

Despite this retail investor rush, real estate speculation ended up being more driven by institutions than individuals. Corporations were soon making more on capital gains from their real estate holdings’ appreciation than from operating profits, which created an urgency to buy up even more property.

Over 38% of real estate purchases between 1984 - 1990 were done by real estate companies who only bought land to quickly flip with little development. These companies were highly leveraged with 44 trillion yen of loans total, a lot of which was lent by shadow banks who were entirely unregulated until 1990.

Speculation also carried over to the stock market. A TINA, ‘there is no alternative’, mindset became pervasive.

Since interest rates remained low and the rising yen discouraged investors from taking their money abroad, the Japanese people were left with no alternative but to continue investing in the domestic stock market.”3

The inflation in the real estate space had an ancillary impact on the stock market as the fashionable pursuit became to look for companies with real estate on the books. Tokyo Electric Power increased in 1986 by a greater market value than all of Hong Kong’s equity value combined. Nippon Airways traded at 1,200x earnings and was a “land play.” Normal business activities were considered irrelevant.

Similar to real estate, stock speculation by companies had an even greater impact than the collective individuals.

"Another unusual feature was the degree to which the bubbles were driven by businesses and banks, rather than by the general public. The volume of trades accounted for by corporations rose from 19% to 39% [during the 1980s], underscoring the extent to which business was responsible for higher levels of speculation."4

The percent of corporations’ stock owned by other companies rose from 39% in 1950 to a whopping 67% in 1980. This was done for speculative reasons but also to tighten relationships with operating partners and help protect against hostile takeovers. This also had the effect of reducing the effective float making share prices easier to manipulate.

A tax law change in 1983 further incentivized corporate speculation (known as Zaitech) by letting companies separate long-term investments and short-term investments with the short-term investment gains taxed at a lower rate than long term. Japanese corporates could also invest in a special “eigyo tokkin” account and get a guaranteed 8%. The amount invested in stocks held in these short term speculative tokkin funds grew from 2 trillion yen in 1983 to 30 trillion in 1987.

On top of the tax advantage, Japanese companies were also allowed to account for the value of their investments at the higher of book cost or market price so they never were forced to mark down an investment yet could flaunt the gains.

How did companies fund this speculation? One way was by issuing “warrant bonds” in the Eurobond market. These were issued in dollars that were subsequently swapped into yen. The yen was expected to appreciate over the life of the bond and could result in a negative interest rate, in other words, the Japanese companies were being paid to borrow money that was purely financing their equity and real estate speculation.

Another source of financing was simply borrowing domestically from banks who were speculating themselves. At the time Japanese banks were allowed to count 45% of their unrealized equity gains towards their capital requirements, so as banks bought up stocks (including other banks' stock) and the equity bubble grew, their capital base expanded which let them lend more and further fuel the bubble.

"A unique feature of these bubbles was the way in which the Japanese financial structure created a self-perpetuating relationship between money and speculation. Banks used land as collateral for lending, so the higher the value of land, the more they could lend. Since unrealized stock profits could be used to fulfill capital requirements, stock price rises also resulted in further extensions of credit. The majority of this borrowed money was then invested in either land or stocks, driving prices even higher and freeing banks to lend even more money, which was in turn invested in land and stocks."5

By the end of the decade, over half of the profit from industrial companies listed on the Tokyo exchange was from speculation. During the second half of the 1980s, while the bubble was raging, operating profits actually declined.

TOPIX index annual returns from 1983, 1984, and 1985 were 23%, 24%, 15%, respectively. Things then really took off in 1986 with the Nikkei up 40% YTD by August, ending the year up 49%. This sharp rise got the public’s attention and further increased interest in the market. The Far Eastern Economic Review declared that “suddenly stocks have become a national street level preoccupation.”

The market had a >20% pull back to start 1987 before being up 60% from mid-1987 through year end. By this point Japanese stocks were worth $4 trillion or almost half the world equity market total.

Euphoric speculation during periods like this are often demonstrated in the IPO market and Japan was no different. First day returns for Japanese IPOs averaged 32% from 1981 – 1991 and in 1988 the average first week return was 74%. In February 1987, the government launched the IPO of Nippon Telephone and Telecom (NTT) with 10 million people applying to get shares (of a 200,000 share issue) before the valuation was even announced. NTT’s share price shot to 200x earnings and the market cap was $376 billion, larger than the stock market value of Germany and Hong Kong combined.

Japanese share prices increased 3x faster than corporate profits (which included the profits from speculation and marking securities up). The textile sector sold for an average of 103x earnings, marine transportation for 176x earnings, fishery and forestry firms for 319x and Japan Air Lines sold at a P/E of 400x.

Shares of companies in the same sectors moved together regardless of differences in earnings and prospects. Shares were hyped for no other reason than that they were “affordable” (read: lower nominal share price) relative to the multi-million-yen NTT price. This is not dissimilar to what we’ve seen recently in the US with new retail traders myopically focused on nominal price. Also similar to the second half of 2020, stock pickers could seemingly do no wrong:

“Shares went up when they issued more shares, when they split shares, when they reported declines in profitability. When Emperor Hirohito died, they went up. When an earthquake struck Tokyo mid-1989, they went up.”6

In the late 1980s, as Western investors became wary of the sky-high valuations and pulled their money out, it was stated that the market was “no longer constrained by Western rationalism with its dry reasoning of discounted cash flows and credit analysis.” The Japanese, on the other hand, accepted the reality disseminated by authority and had no trouble justifying the lofty valuations.

Government Fueled Speculation and Corruption

During the market crash in October 1987, the Ministry of Finance ordered the largest four investment banks to support the stock price of NTT. This was but one instance of the big four banks colluding to “support” certain stocks. Politicians were also frequently given shares that were then pumped by investment banks. This practice was generally known by the public and added further credence to the general populace’s notion that the government would never allow the stock market to fall.

Political venality and openness to bribery was an integral part of the bubble economy. Bureaucrats were pumping stocks and stimulating public interest in equities to try and “help” Japanese companies. While this may sound somewhat well intentioned, corruption became systematic and speculation ran amok because no one in a position of power wanted to step in to control it.

Adding further fuel to the flame, in April 1988 the government abolished tax-exempt postal savings accounts, unleashing an additional $2.25 trillion for new investment into an increasingly illiquid market with the growing corporate cross holdings and low floats created a real share scarcity. In private, the Ministry of Finance officials boasted that, “manipulating the stock market was simpler than controlling the foreign exchange.”

The Japanese tendency to defer to authority and exhibit herding were exploited by banks who pushed certain themes on them that they blindly followed. They hyped untried technologies like cold nuclear fusion and miracle cancer cures. When a Kobe prostitute died of AIDS, a condom maker Sagami Rubber Industries quickly quadrupled. An investment bank advised clients: “A herd instinct is a sound survival instinct in an environment of excess liquidity.”

The Roaring 80s (Absurdities at the Top)

Mortgages were being issued at 2x collateral value and home buyers were taking out 100-year mortgages.

In 1991, real estate in Tokyo cost 40x as much as a comparable property in London. The lifetime earnings of an average office worker were insufficient to buy even a small condo in Tokyo.

Total real estate value in Japan was estimated to be $20 trillion in 1991, 5x that of the entire US and 2x as much as the cumulative value of world's equity markets.

The yakuza were heavily involved in borrowing, speculating and greenmailing bankers and executives and often worked hand in hand with the investment bankers. One such gang leader Susumu Ishii had a 50x return on his investment fund in 1987 and used the proceeds to build a new headquarters at a cost of $113,000 per square meter.

The Bubble Lady, Nui Onoue, was a waitress turned restaurant owner who borrowed an estimated $2 - $ 3 billion in 1987 to speculate in the stock market and became the largest single individual stockholder of many of the largest companies in Japan. She was also a member of a Buddhist cult and would hold all night séances to summon spirits to help her with speculation. She would then tell brokers which stocks to promote the next day and they would oblige. She went bankrupt in 1991 and was left owing $3 billion when the market crashed .

8 million new retail investors entered the stock market in the second half of the 1980s, a nearly 60% increase from the first half.

The newly wealthy were called “shinjinrui” or “the new people” and looked down on those who worked for their wages. Cultural tastes changed with women dressing more scantily, night clubs (and drug use) becoming more popular, an obsession with European designer clothes developed, and a fascination with French cuisine took off in Tokyo.

“The Japanese won’t realize their shares are overvalued as long as they continue paying $300 for a glass of whisky-flavored water in Ginza nightclubs.” – an English stockbroker in Tokyo

During the decade credit card debt increased 3x, total consumer debt increased 7.5x and margin loans grew 8x.

Department stores devoted entire floors to buying and selling stocks and real estate.

A golf club membership bubble developed with over 20 clubs in Japan costing >$1 million to join and the total value of country club memberships estimated to be $200 billion in the late 1980s.

Brokers developed a secondary market for golf club memberships and banks would provide margin against the “collateral” of a golf membership.

Japanese imports of foreign art quadrupled in 1986. A Japanese insurance company paid $40 million for a Van Gogh, topping the previous record paid for a painting by over 3x.

“Paintings have no theoretical value.. Art prices are determined by the meeting of real or induced scarcity with pure irrational desire, and nothing is more manipulable than desire.”

Paintings valued in the multi-millions would by “divided” into $100,000 lots for people who wanted to own a “piece” of a painting. Art became yet another form of collateral banks would accept for borrowers looking to speculate in stocks or real estate.

The record for the most paid for a diamond ($6.4 million) and a book ($5.9 million) were both set in 1987 by Japanese buyers.

By end of 1989 the party was still going with the market up another 27% on the year and 500% for the decade with a P/E ratio of 80x, the dividend yield was 0.38% and the P/B was over 6x.

Some believe that Japanese cultural norms contributed to the bubble lasting as long as it did.

"Commentators at the time often suggested that Japan’s culture of consensus thinking created social reasons not to express pessimistic sentiments about land or stocks. This was compounded by the extent of crossholding, which made it difficult for a corporation to exit the bubble without offending important business partners. The small number of sceptics often went to seemingly absurd lengths to keep a low profile. In September 1990, when Japanese television finally decided to broadcast a panel of bearish financial pundits, the pundits insisted on having their faces blurred out."7

The Crash

At the end of 1989, a new governor of the Bank of Japan was put in place, Yasushi Mieno. He was a career central banker who boasted in public that he had never owned a share of stock. His stated personal mission was to prick the bubble and as with most bubbles, rising interest rates were the tool to pop it. On Christmas day 1989, he raised the official discount rate abruptly to 4.25%, and the Nikkei reached its all-time peak just four days later.

While the market didn’t go into free fall, stocks begin to grind down at the start of 1990:

January: -5%

February: -6%

March: -13%

Stocks stabilized for a few months before collapsing 30% in August and September. By October 1990 the TOPIX was down 46% from its peak ~10 months earlier. The equity price crashes reduced banks' capital reserves which forced them to tighten lending.

Governor Mieno publicly expressed a desire for property prices to fall as well, by a very precise 20%. He raised interest rates five more times very quickly until they reached 6% in August 1990. New regulation was introduced in 1990 limiting loans to real estate companies.

Real estate owners tried to resist selling but ultimately many were forced to. By late 1992, Tokyo real estate prices had fallen by 60%. The fall continued until 1995 when prices leveled out, down 76% and back to ~1980 levels.

The Ministry of Finance had manipulated the market on the way up and with the bubble now popped they tried to control its descent. They reduced margin requirements and restricted new share issuances, they ordered brokers to buy more shares when the Nikkei fell below 20,000 in September 1990, and they restricted life insurance companies from selling shares among other actions. All these measures had little effect on the market and its authorities constant meddling and intervention made the painful aftermath of the bubble that much worse.

Frauds began to be exposed all areas. Golf club membership brokers were caught illegally selling 15x more memberships than prescribed limits and one of the “corporate gangsters” had successfully raised $285 million by selling fraudulent memberships in a public golf course with no private memberships.

All the cheap capital and industry expansion left the country saddled with excess productive capacity.

Trading volume dried up, shrinking 90% from the bubble peak. The party was over.

Aftermath

When the tide went out, the institutional/government abuse came to light. Sumitomo Bank was caught loaning 23 billion yen for the known purpose of market manipulation. Nomura, whose unwritten motto during the decade was reportedly “churn and burn” (referring to retail clients) admitted to pumping shares. Almost all securities companies had been compensating their best clients for losses on stocks with “ambulance shares” (to “heal their wounds”) and multiple former high ranking government officials were busted accepting bribes from property developers and real estate companies.

"A recurring theme in these scandals was the excessively close relationship between the government and the private sector, underlining the bubble’s political roots. The scandal with the most far-reaching consequences was the Recruit scandal of 1988, whereby shares in a human resources firm were offered to politicians prior to their issue in return for favors, implicating the entire cabinet and forcing.”8

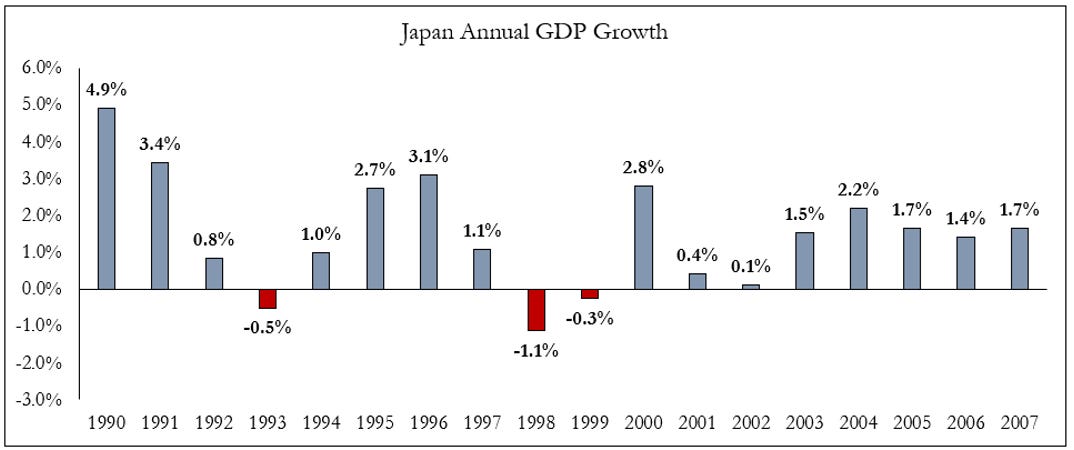

Contrary to conventional wisdom, the bubble popping in 1990 did not began an economic recession. The worst year for GDP growth was -1.1% in 1998 and unemployment never reached > 6%.

However, despite GDP growth holding up initially the financial system was getting wrecked. In 1991, 38% of 12 trillion yen in loans from "shadow banks" were non-performing. By 1995, a full 75% of these loans were non-performing. The government stepped in with bailouts and was successful in avoiding a depression after 60 trillion stimulus or about 11% of Japan's GDP at the time. The majority of this went to covering bad debts. The discount rate was back down to 0.5% by 1995.

"The continued support for failing banks and, by extension, unprofitable businesses had a sclerotic effect on the economy, making it impossible for more efficient firms to compete. The result was a prolonged period of underwhelming economic performance, as the ‘lost decade’ of the 1990s became the ‘lost 20 years.’9

The lasting consequences from the long debt deleveraging (combined with modest population declines) were made evident over the next 20+ years: Japanese GDP in 2017 was only 2.6 per cent higher than it had been in 1997, an annualized growth rate of 0.13%. Lost 20 years, indeed.

Boom Bust. David Turner and William Quinn

Boom Bust. David Turner and William Quinn

Devil Takes the Hindmost. Edward Chancellor

Boom Bust. David Turner and William Quinn

Boom Bust. David Turner and William Quinn

Devil Takes the Hindmost. Edward Chancellor

Boom Bust. David Turner and William Quinn

Boom Bust. David Turner and William Quinn

Devil Takes the Hindmost. Edward Chancellor

Just a couple of percent to bring it all down - lucky we are way smarter now

Good history lesson!